Deferred revenue, also known as unearned revenue is any amount which is earned before the actual revenue is reported. The revenue is deferred to a later date when actual services are performed and hence the name - deferred revenue. Deferred revenue should be identified and shown as an asset until the revenue is recognized in the book of accounts.

For example, a business owner wishes to import machinery worth 100000 INR from USA. The overseas vendor may request part of the sale amount as an advance for processing the order. Lets assume 10000 INR was requested as an advance. This amount will be shown as an asset and then reduced when the invoice is issued and the machinery is received.

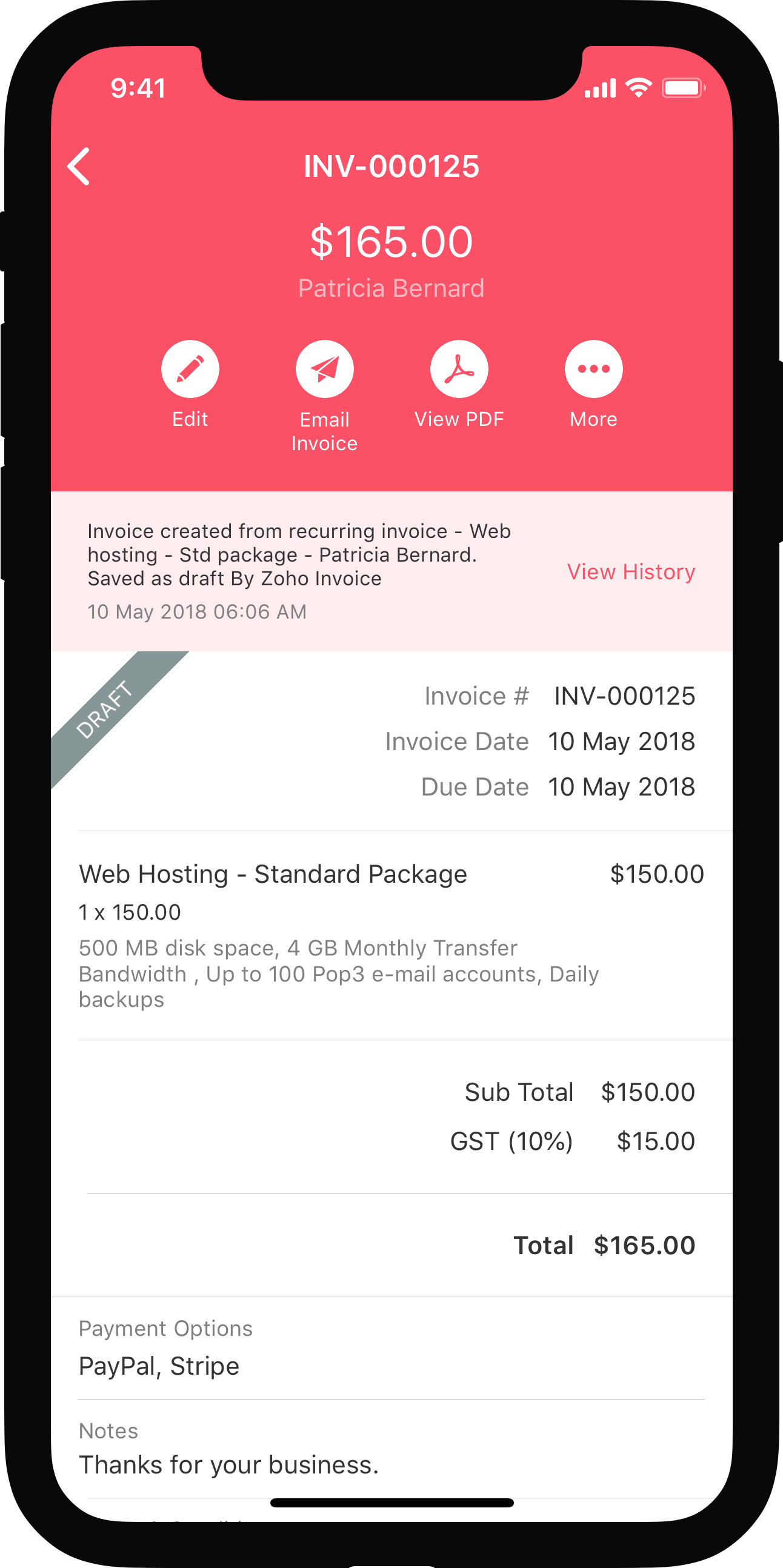

Available in all mobile platforms

Books

One solution for your accounting and GST filing needs